by admin | May 25, 2021 | Corporate Jobs, Employment, Private Jobs

New Delhi : Companies in India are likely to recruit more permanent employees than contractual workers in the times ahead, a report said here on Tuesday.

“The results suggest that recruitment drives will focus more on filling permanent roles, as opposed to temporary or contract positions,” said the “HireRight India Employment Screening Benchmark Report 2018”.

HireRight provides background checking services globally, including for employment and education purposes.

Talking to IANS on the demerits of over-dependence on contractual workers, Steve Girdler, Managing Director of HireRight for EMEA and APAC, said: “Contractors by their very nature are transient – they are employed for a specified length of time and then move on. However, most organisations would regard high turnover as a negative.”

“Not only does this require a constant cycle of training and recruiting, it also becomes difficult to establish a corporate culture and brand when people are constantly coming and going.”

Girdle said that although contract-based workers in a company go through screening process with an agency, the process is not always consistent.

Further, as per the report, “In 2018, almost half (43 per cent) of companies had less than 10 per cent of their workforce made up of non-employee workers.

“This contrasts with the previous year’s findings, where three quarters (73 per cent) of organisations stated that contingent workers accounted for 10 per cent to 19 per cent of their workforce”.

The report also revealed that companies in the country would emphasise on retaining employees in 2018.

“Despite ambitious growth plans, attracting talent appears to be a concern for fewer than half of employers (46 per cent) in India,” it said

“Instead, Indian employers are turning their attentions to minimising turnover, with the number of organisations investing in retention strategies more than doubling from 22 per cent in 2017 to 47 per cent in 2018.”

—IANS

by admin | May 25, 2021 | Business, Economy, Emerging Businesses, Medium Enterprise, News, SMEs

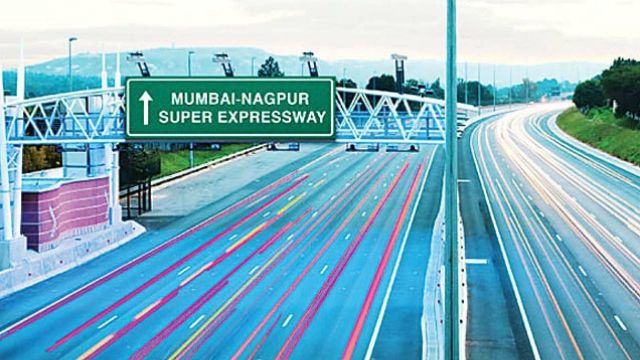

Mumbai : As many as 18 construction majors including Reliance Infrastructure and L&T are in the race for the proposed Rs 46,000-crore Nagpur-Mumbai Super Communication Expressway project, official sources said on Wednesday.

The Maharashtra State Road Development Corp (MSRDC), the nodal agency for the project, opened the financial bids submitted by qualified contractors to construct 13 out of 16 packages of the 700-km long NMSCE.

Bids process for the remaining three packages is still under progress and will be announced later, the sources said.

A pet project of Chief Minister Devendra Fadnavis, the NMSCE, or Maharashtra Samruddhi Mahamarg project, will connect the state capital directly with a high-speed corridor to the second capital in eastern Maharashtra.

The 18 eligible bidders are: Reliance Infrastructure, Megha Eng & Infra Ltd, NCC Ltd, TPL CENGIZ JV, L&T Ltd, Sadbhav Eng Ltd, PNC Infratech Ltd, Afcon Infrastructure Ltd, BSCPL GVPR Jv, Navayuga Eng Co Ltd, APCO Infratech Pvt Ltd, IL&FS Transportation Networks Ltd, KNR Constructions Ltd, Dilip Buildcon Ltd, Montecarlo Ltd, Ashoka Buildcon Ltd, Gayatri Projects Ltd and Oriental Structural Eng Pvt Ltd.

“With the opening of the financial bids, we have achieved a milestone in the implementation of the project. We are now ver close to the historic moment of inauguration,” said MSRDC Vice Chairman and Managing Director Radheshyam Mopalwar.

Mopalwar added that the MSRDC will soon undertake an evaluation of the eligible bids before issuing the work orders and it is expected that the construction work for the NMSCE will begin within the next couple of weeks.

Till date, the state government has acquired 80.25 per cent private and government lands against a total compensation of Rs 4,788-crore for this mega-project.

The NMSCE, a Greenfield Project, will zip through 10 districts, 26 sub-districts and 392 villages en route, reducing the travel time between Mumbai and Nagpur from the existing 18 to just eight hours.

It will help the state prosper through a holistic process that integrates road connectivity with sustainable rural development through agri-business ecosystem and multi-dimensional sub-projects.

—IANS

by admin | May 25, 2021 | Business, Corporate, Corporate Governance, Economy, Emerging Businesses, Investing, Markets, News, Politics

Ranchi : Jharkhand Chief Minister Raghubar Das on Friday laid foundation stone for 151 companies at the fourth groundbreaking ceremony of “Momentum Jharkhand” in Deoghar. These companies will invest Rs 2,700 crore in the state.

Speaking after laying the foundation stone in Deoghar of Jharkhand, the Chief Minister said: “Jharkhand will become a developed state of the country by 2020-2021. In the next 10 years, it will be developed at par with the developed countries.”

The state government had taken several steps to end poverty and generate jobs, he said. The condition of Jharkhand had changed in the last two years as businesses were now investing in the state, he added.

“Prime Minister Narendra Modi will visit Jharkhand on May 24 or 25. Rs 50,000 crore will be invested in the state the day Prime Minister will be here,” he said.

Das said that the Prime Minister would lay the foundation stones for Sindri factory, Adanai ultra power plant in Godda, and for a plastic park and AIIMS in Deoghar.

A number of state ministers, Lok Sabha MPs and legislators were present at the foundation stone laying ceremony.

On Wednesday, Mines and Industries Secretary Sunil Barnawal had said that the Friday’s investment of Rs 2,700-crore investment would create nearly 10,000 direct and 25,000 indirect jobs in the state.

Through Momentum Jharkhand, Rs 8,800 crore had already been invested in the state, which would create around 60,000 direct and 1.75 lakh indirect jobs, he said.

Jharkhand had organised “Momentum Jharkhand: Global Investors’ Summit” in February 2017. The state had received investment proposals worth over Rs 3-lakh crore during the summit.

—IANS

by admin | May 25, 2021 | World

Japan’s Chief Cabinet Secretary Yoshihide Suga

Tokyo : Japan on Friday approved the freezing of assets of additional foreign firms, due to their links with North Korea, which includes adopting new unilateral sanctions.

The sanctions affect four Chinese and two Namibian companies, as well as one Chinese and one North Korean national, adding to the measures announced by Japan in July, a government spokesperson told Efe news.

Tokyo’s decision involves freezing the assets of those believed to be collaborating with the North Korean regime in exporting coal and sending labour abroad, and is meant to curb capital inflows into the rogue nation, in response to its military program escalation.

As a punishment to those associated with the Pyongyang regime’s weapons programs or raw materials trade, Tokyo already included five companies and nine individuals from China on the list in late July.

Japan’s Chief Cabinet Secretary Yoshihide Suga said during a press conference on Friday here, that Japan believes it is extremely important to pressure North Korea, along with the United States and South Korea.

Tokyo’s decision to expand its list comes after Washington announced on Tuesday the freezing of assets and banning financial transactions with more than fifteen Chinese and Russian entities and individuals for their association with North Korea.

Beijing has opposed the imposition of unilateral sanctions by any country outside the framework of the UN.

The UN Security Council approved new sanctions against North Korea earlier this month, imposed for the rogue state’s two intercontinental missile tests in July, which could reduce Pyongyang’s annual export revenue by $1 billion.

—IANS

by admin | May 25, 2021 | Markets, Technology

London:(IANS) When companies go public, they actually innovate more — but their innovations are far more conservative and less ground-breaking than before, new research has found.

“Going public is a mixed bag for firms when it comes to innovation. After an initial public offering, firms tend to introduce a larger number of innovations and a larger variety of each innovation–think different flavours, or different package sizes,” said one of the study authors Simone Wies from Goethe University Frankfurt, Germany.

“But at the same time, the innovations they do make are usually not the kind of breakthrough innovations that take the company in new directions and into new markets,” Wies noted.

The authors analysed a sample of over 40,000 new product introductions by 207 consumer package good (CPG) firms undergoing an initial public offering (IPO) or stock market launch between 1980 and 2011.

They counted each firm’s total new products introduced in a given year.

They then counted the number of new products that could be considered breakthroughs: products that targeted a new market and/or offered a substantially new consumer benefit through product positioning, merchandising, packaging, formulation, or technology.

The authors found that companies pay a price in going public: having to answer to stockholders, who generally are more interested in the short run than the long run, and having now to file cumbersome disclosure reports, companies often find that there is less room for risky and potentially revolutionary innovations.

The findings appeared in the Journal of Marketing Research.